All estate plans share one fundamental goal: create a secure plan that puts beneficiaries in the best possible position. Irrevocable life insurance trusts, known as ILITs, further this goal by protecting your life insurance from the hands of creditors during your lifetime, exempting it from your estate, and reducing your potential estate tax liability. ILITs have many benefits, and very few drawbacks, making them a frequently sought out and powerful estate planning solution. In this article we will discuss the key benefits and drawbacks of ILITs, trustee’s duties, and other key factors.

LIFE INSURANCE & YOUR ESTATE

To understand ILITs, it is important to review exactly what life insurance is, and how life insurance is treated for estate tax purposes. At its core, life insurance is a tool for shifting the financial risk associated with the insured’s death from the family and loved ones onto an insurance company. The mechanics of life insurance are straight forward: the policy owner pays a certain amount to the insurance company called a premium. The premium is often paid monthly, but it can be paid quarterly, annually, or even as a lump sum. In exchange, the insurance company promises to pay a sum to a beneficiary of your choice upon the death of the insured person. While in most cases the insured life and the policy owner are the same person, this is not always the case.

Life insurance payouts received by beneficiaries are not taxed as income for the beneficiary. Rather, the policy is often taxed as part of the deceased’s estate as per I.R.C. § 2042, which states that life insurance is included in the deceased’s estate if the policy is paid to the probate estate, or if the deceased possessed an incident of ownership at death. What this means is that if the insured person was the policy owner, the life insurance payout is included in their taxable estate.

HOW ILITS WORK

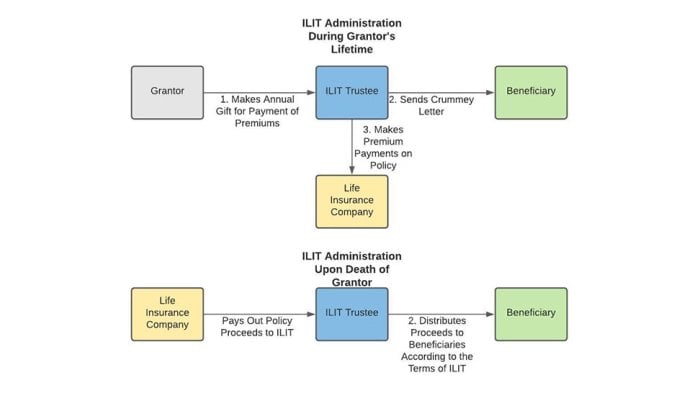

Put simply, an ILIT is an irrevocable trust created for the sole purpose of holding a life insurance policy on the grantor. The trust is generally funded by annual gifts up to the annual gift exclusion ($15,000 in 2020), using the Crummey Letter Method. Once the grantor passes away, the trust collects the life insurance payout and distributes it to the beneficiaries of the trust. To put it within terms of the relevant section of the tax code, an ILIT removes the life insurance from the deceased’s estate because the deceased does not possess an incident of ownership at death. Because the ILIT is irrevocable, the life insurance trust is exempt from your estate, is not accessible to creditors, and any money used to fund it is also removed from your estate, making it an incredibly attractive multi-pronged protective estate planning method.

Like with other irrevocable trusts, the grantor cannot be the trustee of an ILIT. The grantor may freely choose whom they want as their trustee, which can be anyone, including a bank, trust company, attorney, family member, or a trusted friend. One exception is that the grantor cannot choose their spouse as trustee if the life insurance is a survivorship policy, if the trust is funded by jointly held property, or if the gift is made jointly.

An ILIT can protect you and your beneficiaries from creditors or legal judgments against them while the policy is in the trust, since the trust itself is the owner. There can be more than one life insurance policy held in the trust and almost any type of life insurance policy can be held in the trust.

BENEFITS OF AN ILIT

ILITs are excellent estate planning solutions that can accomplish three major objectives for the grantor: Reducing your estate tax bill, protecting your life insurance proceeds from creditors, and protecting your beneficiaries’ inheritance from creditors. If these are goals you are considering as part of your estate plan, an ILIT may be the right solution for you.

AVOIDING ESTATE TAX

Your net estate is the value of your assets minus the value of your debts. Under current federal law, if your net estate is valued at more than $11.58 million per person, you are subject to an estate tax that can be up to 40% of your estate. Even if your estate does not meet the federal limit, you may be subject to a state estate tax. The states that have a state estate tax include:

- Connecticut

- District of Columbia

- Hawaii

- Illinois

- Maine

- Maryland

- Massachusetts

- Minnesota

- New York

- Oregon

- Rhode Island

- Vermont

- Washington

Each of these states sets their own limit of assets excluded from the estate tax, ranging from $1 million to $5.74 million at the time this article was written.

If estate tax is a concern for you, an ILIT takes your life insurance policy and the money used to fund the policy out of your estate valuation, which may be the difference between going over the assets excluded limit under federal or state law.

PROTECTING BENEFICIARIES FROM CREDITORS

ILITs also protect your life insurance proceeds from the hands of creditors and legal judgments. Since the trust is the policyholder, neither the beneficiaries nor you are considered owners of the trust. This means that any of the beneficiaries of the life insurance policy will be secure knowing debts they owe, judgments against them, or any other creditors will not be able to reach the amount they are entitled to from the policy.

ADDITIONAL ADVANTAGES OF AN ILIT

Aside from potentially avoiding estate tax and taking your life insurance policy out of the reach of creditors, ILIT also offers the following benefits:

- Avoid gift taxes – using the Crummey letter method, gift taxes can be avoided if they are at or under $15,000 per person.

- Government benefits – an ILIT can protect a beneficiary who receives government benefits such as security disability income or Medicaid by controlling the payout amount as to not exceed the government limit.

- Avoid generational taxing – if gifting grandchildren, you may be subject to a 40% generational gift tax. Since an ILIT takes the policy out of your net estate it may not be considered a gift and the payout may be disbursed to grandchildren.

- Income tax considerations – the cash value that accumulates in the trust from the policy and the payout are free from taxation during the grantor’s life. However, once the payout is distributed, if it remains in the trust it may be taxed.

WHEN IS AN ILIT NOT THE RIGHT ANSWER?

ILITs offer many benefits; however, they are not for everyone. If you are not concerned about going over the excluded estate tax limit or creditors reaching your life insurance policy, you may be better off with a different type of trust that achieves your specific goals.

Additionally, if you already own a life insurance policy and are concerned about your health, you should be aware of the IRS look back period. This period applies if you transfer an existing life insurance policy into your ILIT. In this case, the IRS will apply a 3 year look back period, meaning that if you die within 3 years of transferring, the policy is still considered part of your taxable estate.

THE ILIT TRUSTEE’S DUTIES

There are three different types of trustees that can be used to administer a trust: individual, bank, and independent trustees. An individual trustee is generally a family member or a friend. A bank trustee is part of a bank trust department and is a professional trustee. An independent trustee is a professional trustee who is not attached to a bank. Independent and bank trustees are professional trustees and charge fees for providing trustee services. However, they are also held to a higher standard of fiduciary duty.

The trustee of an ILIT has five main responsibilities while administering an ILIT:

- Administering the trust

- Sending annual Crummey Letters to beneficiaries

- Payment of life insurance premiums using annual gift

- Filing ILIT tax returns

- Distributing life insurance proceeds upon death of the insured

Deciding on the right approach to protect your assets, secure your estate, and ensure the security of your family is an important decision; one you should discuss with a trusted professional in the field. At Herbert Machinik Law Firm, we’ve helped countless clients protect their financial interests. If you’re ready to learn more about this unique legal arrangement, we are the perfect resource for you and your loved ones.

FREQUENTLY ASKED QUESTIONS ABOUT ILITS

WHAT IS AN IRREVOCABLE TRUST?

An irrevocable trust is trust that cannot be revoked or modified by the grantor once it is created. Irrevocable trusts constitute completed transfers in most cases, and any assets held in an irrevocable trust are not considered part of the grantor’s estate (with some exceptions).

WHAT IS THE CRUMMEY LETTER METHOD?

When you fund your ILIT, you will do so by gifting a certain amount of cash to the trust each year to pay for the insurance premiums. Normally, such gifts would be subject to the gift tax. In order to avoid these gift taxes, your trustee can send out what is known as a “Crummey Letter.” This letter informs beneficiaries that they can ask for their share of the money put in for the premium payment within a certain amount of time. This letter must be sent to all beneficiaries each year letting them know they have immediate access to the money. This will avoid the premium payment being taxed as a gift up to the amount excluded by the federal government. At the time of this article, that is up to $15,000 per giftee.

Beneficiaries must be aware that they cannot actually take the money, otherwise there will not be sufficient funds to cover the premium and the policy will lapse. It is beneficial to let beneficiaries know this ahead of time, and be sure they are aware that the premium payment is minimal compared to what they will receive upon the policy’s payout.

WHAT REQUIREMENTS ARE NECESSARY TO KEEP THE ILIT IN FORCE?

Once your ILIT has been established and you have selected and purchased a life insurance policy, there are a few procedural steps that must be followed to maintain your ILIT. Each year, you will need to transfer cash to the ILIT. Your Trustee will need to notify the beneficiaries of your ILIT using the Crummey Letter method. After the Trustee has gone through the procedural steps necessary for the Crummey method, the Trustee will make the premium payment on the life insurance policy. It may be necessary for your trust to have a separate tax ID number and a separate bank account. It is also possible that your ILIT may require a tax return, though this is unlikely.

HOW DO YOU FUND AN ILIT?

An ILIT is different from many other irrevocable trusts in that it is funded on an ongoing basis. You fund an ILIT by making annual cash gifts using the Crummey Letter Method. The gifts are used to pay the premium on the insurance policy held by the trust.

CAN YOU CHANGE THE BENEFICIARY OF ILIT?

No. An ILIT is an irrevocable trust, and as such the beneficiary cannot be changed by the grantor.

CAN YOU TERMINATE AN ILIT?

An ILIT is an irrevocable trust and therefore it is not possible to terminate it outright. However, there is nothing that compels you to continue funding the ILIT. Thus if you wish to terminate your ILIT, stopping making contributions will achieve the same result, as the trust will be unable to make premium payments on the insurance policy, and the policies will lapse.

CAN YOU FUND AN ILIT WITH AN EXISTING LIFE INSURANCE POLICY?

Yes, although you should be wary of the IRS lookback rule. If you fund an ILIT with an existing policy, the IRS will look back three years, meaning that if you die within three years of funding the ILIT, the policy will be considered part of your estate rather than the ILIT.

WHAT TYPE OF INSURANCE POLICY SHOULD YOU HOLD IN YOUR ILIT?

The most commonly used type of insurance policy will be an individual life policy or a survivorship policy. An individual life policy is simply any policy that insures the life of only one individual. A survivorship policy (also referred to as a second-to-die policy) can only be used if both you and your spouse are still living. A survivorship policy will only pay out a death benefit after both spouses have passed away.